Federal vs Private Student Loans Explained: Which Is Better for College Students in 2026?

Table of Contents

Introduction

Federal vs Private Student Loans Explained is one of the most important topics every college student should understand before borrowing money for higher education.

The cost of attending college has increased significantly over the last two decades. Tuition fees, accommodation expenses, textbooks, transportation, and other educational costs have made college increasingly expensive for students and families.

To bridge the financial gap, millions of students rely on Federal vs Private Student Loans every year.

However, not all Federal vs Private student loans are the same.

Students generally have two major borrowing options:

- Federal Student Loans

- Private Student Loans

Understanding the difference between these two loan types can help students avoid costly financial mistakes and make smarter borrowing decisions.

In this comprehensive guide, we will explain everything college students need to know about federal vs private student loans, including interest rates, eligibility requirements, repayment plans, advantages, disadvantages, and long-term financial impacts.

What Are Federal vs Private Student Loans?

A student loan is money borrowed specifically to pay educational expenses.

Unlike scholarships and grants, Federal vs Private student loans usually must be repaid with interest.

Students often use loans to cover:

- Tuition fees

- Housing expenses

- Meal plans

- Books and supplies

- Transportation costs

- Technology expenses

- Living expenses

Federal vs Private Student loans make higher education accessible to millions of students who otherwise could not afford college.

Why Understanding Federal vs Private Student Loans Is Important

Many students borrow money without fully understanding the consequences.

Unfortunately, poor borrowing decisions can lead to years of financial stress after graduation.

Understanding Federal vs Private student loans helps students:

Borrow Responsibly

Students can avoid unnecessary debt.

Compare Financing Options

Different loans offer different benefits.

Reduce Repayment Costs

Choosing the right loan can save thousands of dollars.

Protect Future Financial Health

Better loan decisions improve long-term financial stability.

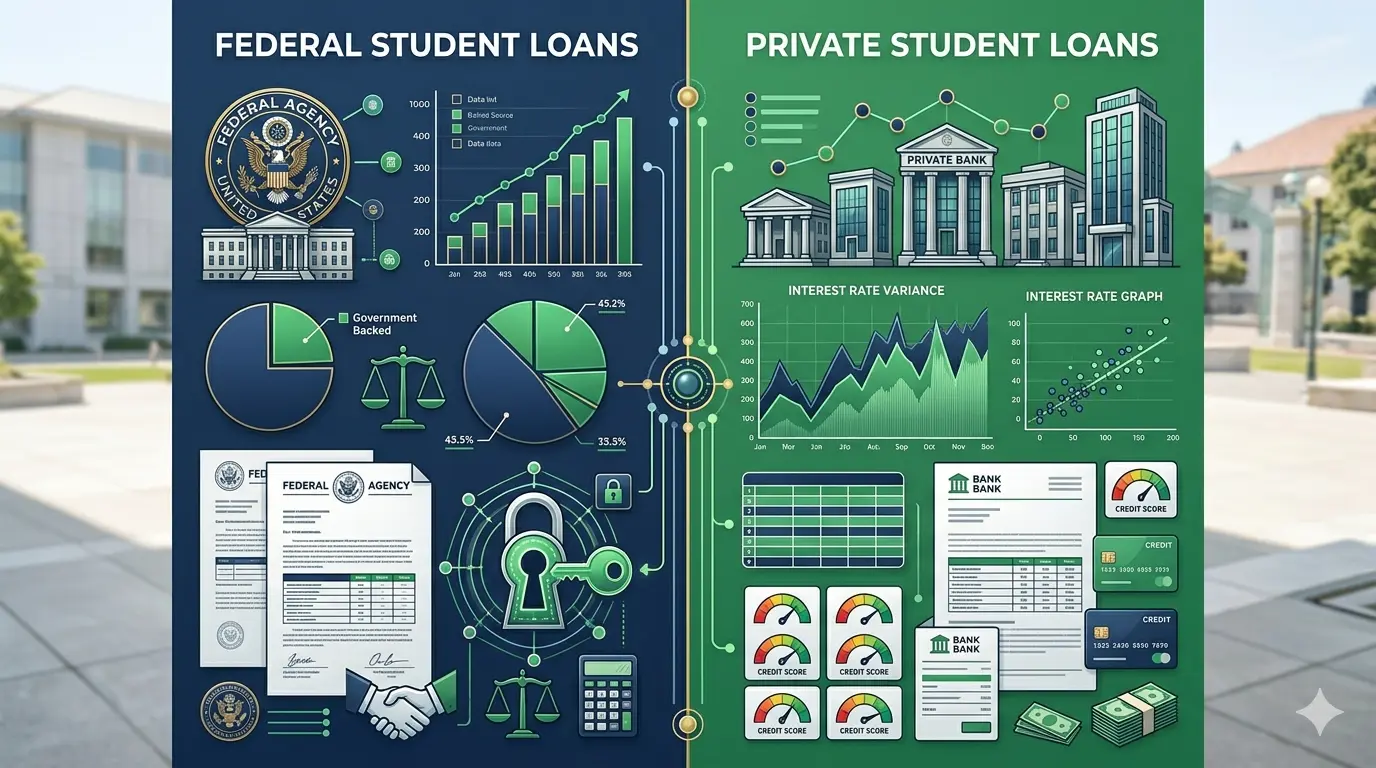

Overview of Federal Student Loans

Federal student loans are provided by the U.S. federal government.

They are generally considered the best starting point for students because they offer borrower protections that private loans usually do not provide.

Most financial aid experts recommend exhausting federal loan options before considering private student loans.

Key Characteristics of Federal Student Loans

Federal student loans typically offer:

- Fixed interest rates

- Flexible repayment plans

- Loan forgiveness opportunities

- Government protections

- No credit requirements for many programs

These benefits make federal loans attractive for many students.

Types of Federal Student Loans

There are several federal loan programs available.

Direct Subsidized Loans

Direct Subsidized Loans are available to undergraduate students with demonstrated financial need.

One of the biggest advantages is that the government pays interest while the student is enrolled at least half-time.

Benefits include:

- Lower overall borrowing costs

- Financial need consideration

- Government-paid interest during eligible periods

Many students prioritize subsidized loans first.

Direct Unsubsidized Loans

Direct Unsubsidized Loans are available to:

- Undergraduate students

- Graduate students

- Professional students

Unlike subsidized loans, interest begins accumulating immediately.

Benefits include:

- Wider eligibility

- No financial need requirement

- Available to graduate students

However, accumulated interest can increase total repayment costs.

Direct PLUS Loans

PLUS Loans are designed for:

- Parents of dependent undergraduate students

- Graduate students

- Professional students

These loans often allow higher borrowing limits.

However, they may have higher costs compared to some other federal loan options.

What Is FAFSA?

One of the most common questions students ask is:

“What is FAFSA?”

FAFSA stands for:

Free Application for Federal Student Aid

Students must complete FAFSA to determine eligibility for federal financial aid programs.

FAFSA may qualify students for:

- Grants

- Scholarships

- Work-study programs

- Federal student loans

Students can learn more through the Federal Student Aid website:

DoFollow External Resource:

https://studentaid.gov

Benefits of Federal Student Loans

Federal student loans provide several significant advantages.

Fixed Interest Rates

Federal loans typically use fixed interest rates.

This means:

Your interest rate remains unchanged throughout the repayment period.

Predictable payments make budgeting easier.

Income-Driven Repayment Plans

Federal borrowers may qualify for income-driven repayment plans.

Payments are based on:

- Income

- Family size

- Financial situation

This flexibility helps borrowers experiencing financial challenges.

Loan Forgiveness Opportunities

Certain federal borrowers may qualify for forgiveness programs.

Examples include:

- Public Service Loan Forgiveness

- Teacher Loan Forgiveness

These programs may reduce long-term debt obligations.

Deferment and Forbearance Options

Federal loans often provide relief during financial hardship.

Borrowers may temporarily pause payments under qualifying circumstances.

Overview of Private Student Loans

Private student loans are offered by:

- Banks

- Credit unions

- Online lenders

- Financial institutions

Private lenders evaluate risk differently than federal programs.

Approval often depends on:

- Credit score

- Income

- Employment history

- Cosigner strength

Private loans can be useful but require careful evaluation.

Why Students Consider Private Student Loans

Federal aid may not always cover the full cost of attendance.

Students often turn to private lenders when:

Tuition Exceeds Federal Limits

Educational costs may exceed available federal funding.

Graduate School Expenses Increase

Advanced degrees often require additional financing.

Specialized Programs Cost More

Professional education may involve substantial expenses.

Private loans can help close funding gaps.

Key Characteristics of Private Student Loans

Private student loans differ significantly from federal loans.

Common features include:

- Credit-based approval

- Variable or fixed rates

- Limited government protections

- Cosigner requirements

- Different lender terms

Students should compare lenders carefully before borrowing.

Federal vs Private Student Loans: Basic Comparison

| Feature | Federal Loans | Private Loans |

|---|---|---|

| Source | Government | Banks & Lenders |

| Credit Check | Usually No | Usually Yes |

| Fixed Rates | Yes | Often |

| Variable Rates | No | Available |

| Income-Based Repayment | Yes | Rare |

| Loan Forgiveness | Available | Rare |

| Government Protection | Strong | Limited |

| Cosigner Needed | Usually No | Often Yes |

This comparison highlights why federal loans are generally recommended first.

Internal Links to Add

Within this article, link to:

Best Federal vs Private Student Loans for College Students in USA

FAFSA Complete Guide

Student Loan Repayment Plans Explained

These internal links improve SEO and user experience.

Interest Rates Explained: Federal vs Private Student Loans

One of the biggest differences between Federal vs Private student loans is the interest rate structure.

Interest rates directly affect:

- Monthly payments

- Total repayment costs

- Long-term debt burden

Even a small difference in interest rates can cost borrowers thousands of dollars over time.

What Is an Interest Rate?

An interest rate is the cost of borrowing money.

When you borrow a student loan, you repay:

- Original loan amount (principal)

- Interest charged by the lender

The higher the interest rate, the more expensive the loan becomes.

Federal Student Loan Interest Rates

Federal student loan rates are set by the U.S. government.

Benefits include:

Fixed Rates

Federal loans generally have fixed interest rates.

This means:

Your rate remains the same throughout repayment.

Advantages:

- Predictable monthly payments

- Easier budgeting

- Protection from rising interest rates

Example

Suppose you borrow:

$20,000

At a fixed interest rate.

Your rate remains unchanged regardless of market conditions.

This stability helps borrowers plan financially.

Private Student Loan Interest Rates

Private lenders offer:

Fixed Interest Rates

OR

Variable Interest Rates

Borrowers may choose between the two.

Variable Interest Rates

Variable rates change based on market conditions.

Benefits:

- Lower initial rates

Risks:

- Payments may increase later

- Higher long-term costs

Students should understand these risks before choosing a variable-rate loan.

Which Interest Rate Option Is Better?

For most college students:

Fixed rates offer greater financial security.

Variable rates may work for borrowers who:

- Expect higher future income

- Plan rapid repayment

- Understand market risks

Most financial advisors recommend caution with variable-rate loans.

Eligibility Requirements

Another major difference involves loan qualification.

Federal and private loans use different approval standards.

Federal Student Loan Eligibility

Federal loans focus primarily on educational eligibility rather than credit history.

Students generally need:

- U.S. citizenship or eligible status

- Enrollment in an eligible institution

- FAFSA completion

- Satisfactory academic progress

Most undergraduate students can qualify.

No Credit Score Requirement

One major advantage:

Many federal loans do not require a credit check.

This benefits students with:

- No credit history

- Limited financial experience

Federal aid remains accessible to many borrowers.

Private Student Loan Eligibility

Private lenders assess financial risk more carefully.

Approval often depends on:

Credit Score

Higher scores improve approval chances.

Income

Lenders evaluate repayment ability.

Employment History

Stable income can improve eligibility.

Debt-to-Income Ratio

Existing debt may affect approval.

Cosigner Requirements

Many students lack sufficient credit history.

As a result, private lenders often require a cosigner.

A cosigner may be:

- Parent

- Guardian

- Relative

Strong cosigners may help secure:

- Better rates

- Higher approval odds

- Larger loan amounts

Understanding FAFSA Benefits

The FAFSA is one of the most important financial aid tools available to students.

FAFSA stands for:

Free Application for Federal Student Aid

Students can apply here:

External Resource (DoFollow):

https://studentaid.gov/h/apply-for-aid/fafsa

Why FAFSA Matters

Many students incorrectly assume they won’t qualify.

However, FAFSA may unlock access to:

- Grants

- Scholarships

- Work-study programs

- Federal student loans

Even middle-income families should apply.

FAFSA Benefits Beyond Loans

FAFSA provides opportunities beyond borrowing.

Pell Grants

Pell Grants generally do not require repayment.

This reduces student debt.

Institutional Aid

Many colleges use FAFSA data to award aid.

Students who skip FAFSA may miss valuable opportunities.

State-Based Aid

Some states require FAFSA completion for assistance programs.

This increases available funding sources.

Private Loan Approval Process

Private loan applications are typically more detailed than federal aid applications.

Step 1: Application Submission

Students provide:

- Personal information

- School information

- Financial details

Step 2: Credit Evaluation

Lenders review:

- Credit score

- Credit history

- Existing obligations

Step 3: Cosigner Review

If necessary, lenders evaluate the cosigner’s finances.

Step 4: Approval Decision

Approved borrowers receive loan offers containing:

- Interest rates

- Repayment terms

- Loan limits

Students should compare offers carefully.

Federal vs Private Repayment Plans

Repayment flexibility is one of the most important differences between loan types.

Federal Repayment Plans

Federal loans offer multiple repayment options.

Standard Repayment Plan

Characteristics:

- Fixed monthly payments

- Predictable schedule

Often results in lower total interest costs.

Graduated Repayment Plan

Payments begin lower and increase over time.

Useful for:

- Early-career professionals

- Graduates expecting income growth

Extended Repayment Plan

Longer repayment terms reduce monthly payments.

However:

Total interest costs increase.

Income-Driven Repayment Plans

One of the strongest federal loan benefits.

Payments depend on:

- Income

- Family size

- Financial circumstances

Learn more:

External Resource (DoFollow):

https://studentaid.gov/manage-loans/repayment/plans

Advantages of Income-Driven Repayment

Benefits include:

Affordable Payments

Monthly obligations remain manageable.

Financial Flexibility

Helpful during career transitions.

Potential Forgiveness

Some balances may qualify for forgiveness after meeting requirements.

Private Loan Repayment Plans

Private lenders usually offer fewer repayment options.

Repayment structures vary by lender.

Common plans include:

- Immediate repayment

- Interest-only payments

- Deferred repayment

Students should review terms carefully.

Federal Loan Forgiveness Programs

Loan forgiveness is one of the most valuable federal benefits.

Public Service Loan Forgiveness (PSLF)

Available for eligible public service employees.

Examples:

- Government workers

- Nonprofit employees

- Certain educators

Eligible borrowers may receive remaining balance forgiveness after meeting program requirements.

Teacher Loan Forgiveness

Certain teachers may qualify for forgiveness benefits.

Eligibility depends on:

- Subject area

- School location

- Years of service

These programs can significantly reduce debt.

Private Loan Forgiveness Availability

Private lenders rarely offer forgiveness programs.

Borrowers generally remain responsible for full repayment.

This is a significant difference compared to federal loans.

Real-World Example #1

Student A

Federal Loan Borrower

Benefits:

- Fixed rates

- Income-driven repayment

- Forgiveness eligibility

Financial flexibility remains high.

Student B

Private Loan Borrower

Benefits:

- Larger loan amount

- Fast approval

Challenges:

- Fewer protections

- Potentially higher risk

This example highlights why federal aid is often recommended first.

Real-World Example #2

A student needs:

$30,000

for educational expenses.

Available options:

Federal Loan

Rate fixed by government.

Includes:

- Flexible repayment

- Forgiveness opportunities

Private Loan

Variable rate offered.

May start lower but increase later.

Understanding long-term costs becomes critical.

Common Borrowing Mistakes

Students frequently make avoidable errors.

Borrowing Too Much

Only borrow what is necessary.

Ignoring Interest Accumulation

Interest can significantly increase repayment costs.

Choosing Based Only on Monthly Payment

Lower payments often mean longer repayment periods.

Not Completing FAFSA

Students may lose access to valuable aid.

Internal Links to Add

Within this section, link to:

- Best Student Loans for College Students in USA

- FAFSA Complete Guide

- Student Loan Repayment Plans Explained

- Personal Finance Tips for College Students

These internal links improve user experience and SEO performance.

Best Private Student Loan Lenders to Consider

After exhausting federal student aid, many students explore private student loan options.

Private lenders vary significantly in:

- Interest rates

- Repayment flexibility

- Borrowing limits

- Cosigner policies

- Customer service

Comparing lenders carefully can save thousands of dollars over the life of a loan.

Features of a Good Student Loan Lender

Before choosing a private lender, students should evaluate:

Competitive Interest Rates

Lower rates reduce overall borrowing costs.

Flexible Repayment Terms

Borrowers benefit from repayment options that adapt to financial circumstances.

Cosigner Release Options

Some lenders allow cosigners to be removed after consistent on-time payments.

Hardship Assistance Programs

Financial difficulties can occur unexpectedly.

Lenders offering hardship support provide additional security.

Federal vs Private Student Loan Cost Comparison

The true cost of a student loan extends beyond the amount borrowed.

Students should compare:

- Interest rates

- Fees

- Repayment terms

- Total interest costs

- Borrower protections

Example Scenario

Student borrows:

$25,000

Federal Loan

- Fixed interest rate

- Income-driven repayment eligibility

- Loan forgiveness potential

Private Loan

- Credit-based approval

- Variable or fixed rates

- Limited borrower protections

Over a decade or longer, total repayment costs can differ significantly.

Understanding Annual Percentage Rate (APR)

Many students focus only on interest rates.

However, APR provides a more complete borrowing cost picture.

APR includes:

- Interest charges

- Certain lender fees

Comparing APR helps students identify the most affordable loan option.

Student Loan Refinancing Explained

Refinancing means replacing one or more existing loans with a new loan.

Borrowers often refinance to:

- Reduce interest rates

- Lower monthly payments

- Simplify repayment

Benefits of Refinancing

Refinancing may provide:

Lower Interest Costs

Reduced rates can save substantial money.

Simplified Debt Management

Multiple loans become one loan.

Improved Monthly Cash Flow

Lower payments can ease financial pressure.

Risks of Refinancing Federal Loans

Students must understand a major drawback.

Refinancing federal loans into private loans may eliminate access to:

- Income-driven repayment plans

- Public Service Loan Forgiveness

- Federal borrower protections

- Deferment benefits

This decision should be evaluated carefully.

When Should You Refinance?

Refinancing may make sense if:

Credit Score Has Improved

Better credit often leads to lower rates.

Income Is Stable

Lenders favor financially stable borrowers.

Existing Rates Are High

Lower market rates may create savings opportunities.

Student Loan Consolidation vs Refinancing

Many borrowers confuse these terms.

Consolidation

Typically applies to federal loans.

Benefits:

- Single monthly payment

- Simplified management

Federal protections remain intact.

Refinancing

Usually involves a private lender.

Benefits:

- Potentially lower rates

Possible disadvantage:

- Loss of federal benefits

Understanding the difference is important.

Federal vs Private Student Loans: Pros and Cons

Federal Student Loan Advantages

Easier Qualification

Most students can qualify.

Fixed Interest Rates

Predictable repayment.

Income-Driven Repayment

Payments based on earnings.

Loan Forgiveness Programs

Potential debt reduction opportunities.

Strong Borrower Protections

Government-backed safeguards.

Federal Student Loan Disadvantages

Borrowing Limits

Students may not receive enough funding.

Application Requirements

FAFSA completion is necessary.

Funding Restrictions

Certain expenses may exceed available aid.

Best Colleges for Diploma Courses in the USA (2025 Ultimate Guide)

Private Student Loan Advantages

Higher Borrowing Limits

Can cover remaining educational costs.

Competitive Rates for Qualified Borrowers

Excellent credit may secure favorable terms.

Faster Processing

Some lenders offer rapid approvals.

Flexible Loan Structures

Multiple repayment choices may exist.

Private Student Loan Disadvantages

Credit Requirements

Approval often depends on creditworthiness.

Cosigner Requirements

Many students need assistance qualifying.

Fewer Protections

Limited hardship and forgiveness options.

Variable Rate Risk

Future payment increases may occur.

Student Loan Debt Reduction Strategies

Responsible repayment can reduce long-term costs.

Strategy 1: Pay Interest During School

For unsubsidized loans:

Interest begins accruing immediately.

Making interest payments while enrolled prevents balance growth.

Strategy 2: Make Extra Payments

Additional payments reduce:

- Principal balance

- Interest expenses

- Repayment duration

Even small extra payments help.

Strategy 3: Use Automatic Payments

Many lenders offer rate discounts for autopay enrollment.

Benefits include:

- Lower rates

- Improved payment consistency

Strategy 4: Create a Repayment Budget

Graduates should include student loans within a broader financial plan.

Track:

- Income

- Housing expenses

- Transportation

- Savings

- Debt obligations

Budgeting improves financial stability.

Student Loan Impact on Credit Scores

Student loans affect credit history.

Responsible management can strengthen financial standing.

Positive Credit Effects

On-time payments may:

- Build credit history

- Improve credit scores

- Increase future borrowing opportunities

Negative Credit Effects

Missed payments may result in:

- Credit damage

- Collection actions

- Higher future borrowing costs

Payment discipline remains essential.

USA vs UK Student Loan Systems

Many international students compare education financing systems.

While both countries support higher education access, important differences exist.

United States Student Loan System

Characteristics include:

- Federal loans

- Private loans

- FAFSA-based aid

- Multiple repayment options

Students often combine various funding sources.

United Kingdom Student Loan System

Characteristics include:

- Government-administered funding

- Income-based repayment thresholds

- Different tuition funding structures

Repayment rules differ substantially from the U.S. model.

Which System Is Better?

Each system offers unique benefits.

The best choice depends on:

- Educational goals

- Residency status

- Career plans

- Financial circumstances

Students should research their options thoroughly.

Student Loan Return on Investment (ROI)

Before borrowing, students should evaluate educational ROI.

Questions to ask:

What Career Opportunities Exist?

Job demand affects earning potential.

What Is the Average Salary?

Expected income influences repayment affordability.

How Much Debt Is Required?

Higher debt increases financial risk.

Is the Degree in Demand?

Growing industries often provide stronger opportunities.

High-ROI Degree Fields

Historically, strong returns have been associated with:

Engineering

High demand and competitive salaries.

Computer Science

Technology careers continue expanding.

Healthcare

Many healthcare professions remain essential.

Finance

Strong earning potential and career growth.

Data Analytics

Growing importance across industries.

Common Student Loan Myths

Many students misunderstand how borrowing works.

Myth 1: Student Loans Are Free Money

Reality:

Loans must usually be repaid with interest.

Myth 2: Monthly Payments Don’t Matter Until Graduation

Reality:

Repayment planning should begin before borrowing.

Myth 3: Private Loans Are Always Better

Reality:

Federal loans often provide stronger protections.

Myth 4: More Borrowing Is Better

Reality:

Only borrow what is necessary.

Expert Recommendations

Financial experts frequently suggest:

Complete FAFSA Every Year

Many students miss valuable aid opportunities.

External Resource (DoFollow):

https://studentaid.gov/h/apply-for-aid/fafsa

Prioritize Scholarships and Grants

These forms of aid generally do not require repayment.

Use Federal Loans First

Federal protections provide significant advantages.

Compare Multiple Lenders

Never accept the first private loan offer without comparison.

Understand Every Loan Document

Read terms carefully before signing.

Internal Links to Add

Throughout Part 3, link to:

Best Student Loans for College Students in USA

FAFSA Complete Guide

Student Loan Repayment Plans Explained

Personal Finance Tips for College Students

How to Build Credit Score as a Student

These internal links strengthen SEO and improve user navigation.

Final Verdict: Federal vs Private Student Loans Explained

For most students, Federal vs Private student loans should be the first financing option considered.

Federal loans generally provide:

✓ Fixed interest rates

✓ Flexible repayment plans

✓ Loan forgiveness opportunities

✓ Strong borrower protections

✓ Easier qualification requirements

Federal vs Private student loans can still play an important role when federal aid is insufficient. However, borrowers should compare lenders carefully and fully understand the long-term financial implications before committing.

The best borrowing strategy typically involves:

- Completing FAFSA

- Maximizing scholarships and grants

- Using federal loans first

- Considering private loans only when necessary

- Borrowing responsibly

- Planning repayment before graduation

Conclusion

Understanding the differences between federal and private student loans is the first step toward making smart financial decisions for college. Federal student loans typically provide stronger protections, fixed interest rates, income-driven repayment plans, and potential loan forgiveness opportunities. Private student loans can help fill funding gaps but often come with stricter approval requirements and fewer borrower protections.

For most students, federal loans should be considered before exploring private loan options. However, every financial situation is unique, making research and comparison essential.